Intimidation Threat

Intimidation threat: This may occur when a chartered accountant may be deterred from action objectively by threats, actual or perceived.

- Being threatened with dismissal or replacement in relation to a client engagement.

- Being threatened with litigation.

- Being pressured to reduce inappropriately the extent of work performed in order to reduce fees.

[wpipa id=”616″]

Mr.A was the audit manager during the last year’s annual audit of ABC Limited. He has joined ABC Limited as their Manager Finance, prior to the commencement of the current year’s audit.

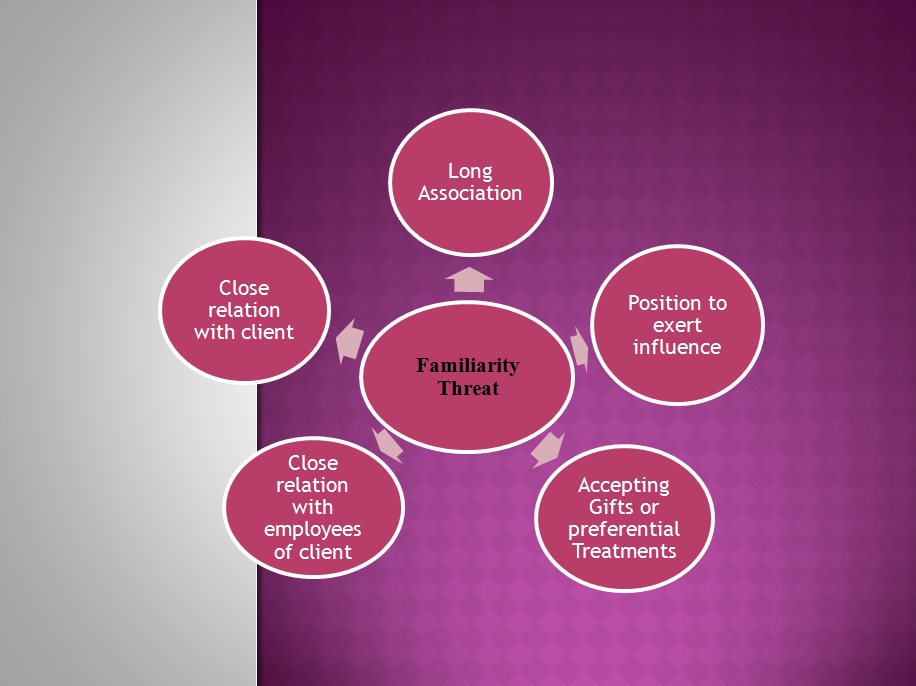

Threats: It has created self interest (Self Interest Threat to Auditor and related Safeguards) familiarity(Familiarity Threat to auditor and related Safeguards) and intimidation threats. The assurance team’s independence is threatened, on account of the fact that Mr.A is in a position to exert direct and significant influence over the assurance engagement as Mr.A was a member of the assurance team during the previous year audit.

Threats: It has created self interest (Self Interest Threat to Auditor and related Safeguards) familiarity(Familiarity Threat to auditor and related Safeguards) and intimidation threats. The assurance team’s independence is threatened, on account of the fact that Mr.A is in a position to exert direct and significant influence over the assurance engagement as Mr.A was a member of the assurance team during the previous year audit.

Safeguards: The safeguards might include:

- Consider the appropriateness or necessity of modifying the assurance plan for the assurance engagement;

- Assigning an assurance team that is of sufficient experience in relation to the individual who has joined the assurance client;

- Involve an additional chartered accountant who was not a member of the assurance team to review the work or advise as necessary; or

- Quality control review of the assurance engagement

- Ensuring that the individual concerned is not entitled to any benefits or payments from the firm unless these are made in accordance with fixed predetermined arrangements. In addition, any amount owed to the individual should not be of such significance to threaten the firm’s independence.

- Ensuring that the individual does not continue to participate or appear to participate in the firm’s business or professional activities.

Your firm is the auditor of Prime Super Markets Limited, a chain of super markets. During a promotional campaign, the management has distributed discount vouchers which have also been given to the audit team members.

Ans.Accepting of discount vouchers may create self interest and intimidation threats. However, if the value of discount vouchers is not clearly insignificant, the threat to independence cannot be reduced to an acceptable level by the application of any safeguard. If the value is other than clearly insignificant, the members of the audit team should be instructed not to accept the discount vouchers.

Auditor forum has also discussed remaining types of threat through links:

Advocacy threat with examples and related safeguards

Self Interest Threat to Auditor and related Safeguards

Familiarity Threat to auditor and related Safeguards

Self Review Threat with examples and real life situations

For more practicing questions and answers related to threats and safeguards in real life situations explore auditorforum.com We are keen to know your views in comments.

{kind=link}