Unique Enterprises is a large scale manufacturer of mobile parts and accessories. It has acquired a new ERP to integrate different departments. It is also planning to connect with its …

List the important matters that are required to be included in an audit engagement letter. Ans. Key Components of Audit engagement letter: The objective and scope of the audit of …

Internal Audit vs External Audit List the important differences between internal audit and external audit with respect to the following: (i) Independence (ii) Objectives (iii) Reporting Important differences between Internal Audit …

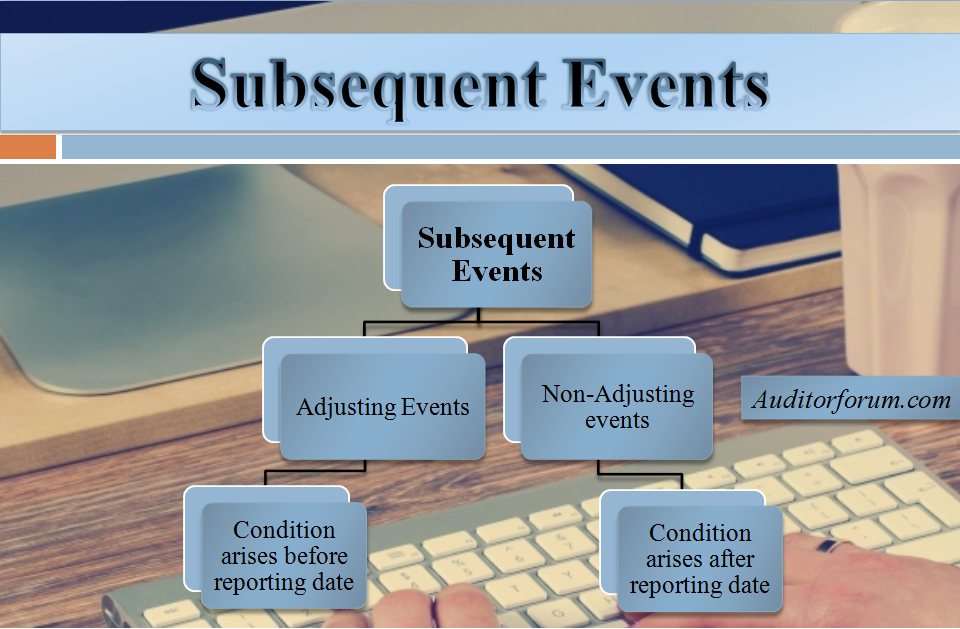

What are Subsequent Events? Definition: Events favorable or unfavorable occurred between the end of the reporting period and the date when financial statements are authorized for issue are called Subsequent Events. Types …

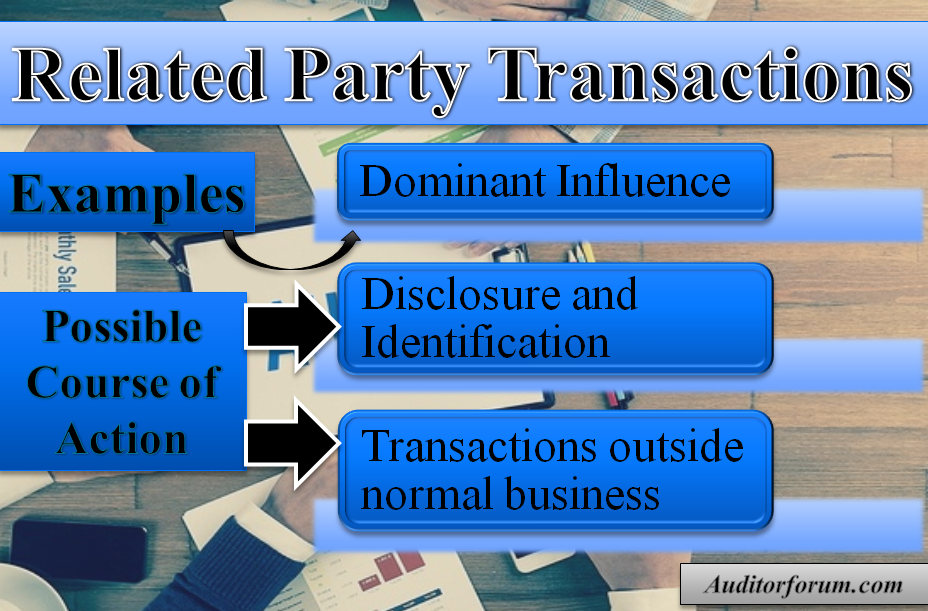

What are the situations that may be indicative of dominant influence exerted by a related party. Indicators of dominant influence exerted by a related party include the following: Significant transactions are …