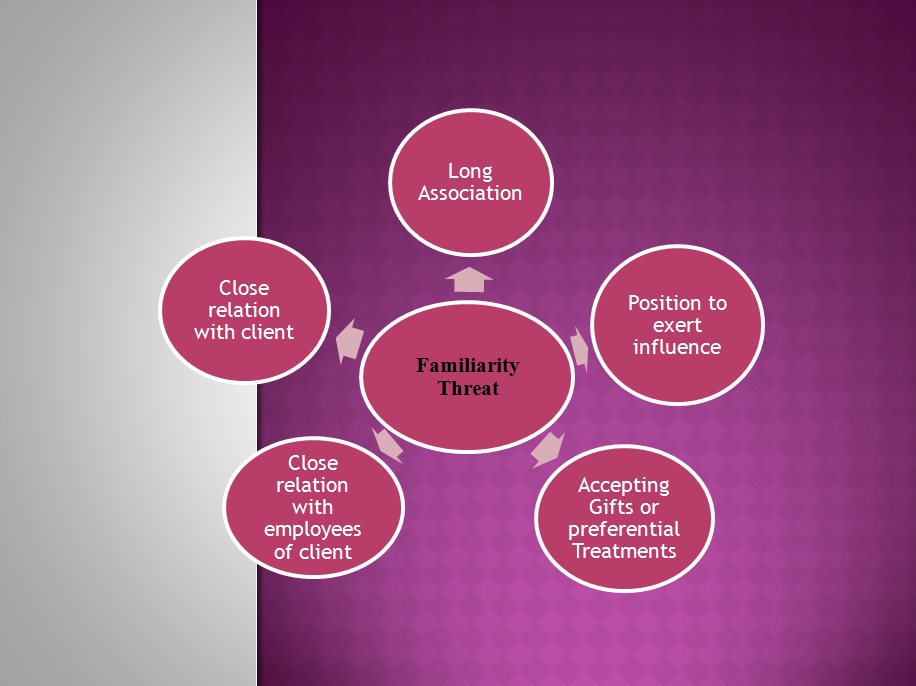

Self-Interest Threat: self interest threat may occur as a result of the financial or other interests of a chartered accountant or of an immediate or close family member.

- A financial interest in a client or jointly holding a financial interest with a client

- Undue dependence on total fees from a client

- Having a close business relationship with a client

- Concern about the possibility of losing a client

- Potential employment with a client

- Contingent fees relating to an assurance engagement

- A loan to or from an assurance client or any of its directors or officers

Q. It has been discovered that father of one of the trainees posted on the audit of CL, has a financial interest in CL.

Ans. In the given situation involvement of such trainees in the audit of CL may result in a self-interest threat. The materiality and significance of the financial interest, needs to be evaluated. If the financial interest is immaterial then the audit trainee may be allowed to work on that client, otherwise only safeguard available is to withdraw the trainee from this assignment.

[wpipa id="616"]

Q. HL, an audit client of your firm has recently advertised certain vacancies in its accounts department. The said positions have been applied for by number of individuals including two staff members who are posted on the audit of HL.

Ans. A self interest threat is created when a member of the assurance team participates in the assurance engagement while knowing, or having reason to believe, that he may join the assurance client in future. The threat created can be reduced to an acceptable level by the application of the following safeguards:

1.Ask the individual to notify the firm when entering serious employment negotiations with the assurance client;

2.Remove of the individual from the assurance engagement;

3.Perform an independent review of any significant judgments made by that individual while on engagement.

Q. During the course of audit of HP Limited (HPL), the engagement partner has informed the firm that his brother has acquired 200,000 shares in HPL.

Threats: Self interest threat is created as the shares are held by a close relative of the engagement partner. As the engagement partner has promptly notified the firm about the interest of his brother, hence it is likely that it would not impair the independence of the engagement partner.

[wpipa id="616"]

Safeguards: Significance of threat should be evaluated and if the threat is other than clearly insignificant, safeguards should be considered and applied as necessary to reduce the threat to an acceptable level. Such safeguards might include:

1.If possible the engagement partner may convince his brother to dispose of the shares;

2.If the disposal does not occur at the earliest practical date, the engagement partner may be changed.

3.An additional chartered accountant who did not take part in the assurance engagement may review the work done or otherwise advise as necessary.

For more practicing questions and answers related to threats and safeguards in real life situations explore auditorforum.com We are keen to know your views in comments.

{kind=link}