Analytical procedures: It consist of evaluations of financial information through analysis of plausible relationships among financial as well as non-financial data. Analytical procedures also encompass investigation of identified fluctuations or relationships that are inconsistent with other relevant information or that differ from expected values by a significant amount.

Examples Of Analytical Procedures

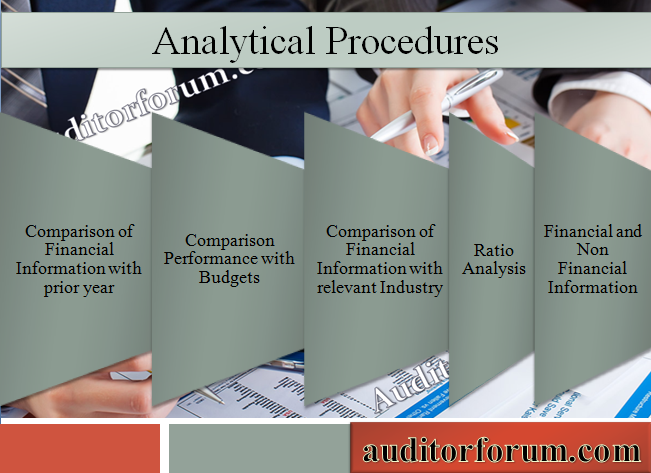

Examples of analytical procedures:

- Comparison of the entity’s financial information with comparable information for prior periods.

- Comparison of the entity’s financial information with anticipated results of the entity, such as budgets or forecasts, or expectations of the auditor, such as an estimation of depreciation.

- Comparison of the entity’s financial information with similar industry information, such as a comparison of the entity’s ratio of sales to accounts receivable with industry averages or with other entities of comparable size in the same industry.

- Consideration of relationships among elements of financial information that would be expected to conform to a predictable pattern based on the entity’s experience, such as gross margin percentages.

- Consideration of relationships between financial information and relevant nonfinancial information, such as payroll costs to number of employees

State with examples the factors that are relevant in assessing the reliability of data for the purposes of designing substantive analytical procedures.

The following factors are relevant in determining the reliability of data while designing substantive analytical procedures:

- Source of the information available. For example, information may be more reliable when it is obtained from independent sources outside the entity;

- Comparability of the information available. For example, broad industry data may need to be supplemented to be comparable to that of an entity that produces and sells specialized products;

- Nature and relevance of the information available. For example, whether budgets have been established as results to be expected rather than as goals to be achieved; and

- Controls over the preparation of the information that are designed to ensure its completeness, accuracy and validity. For example, controls over the preparation, review and maintenance of budgets.

Specify the procedures that an auditor may undertake if analytical procedures identify inconsistencies with other information.

If analytical procedures identify fluctuations or relationships that are inconsistent with other relevant information, the auditor shall investigate such differences by:

- Inquiring of management and obtaining appropriate audit evidence relevant to management’s responses; and

- Performing other audit procedures as necessary in the circumstances.

Auditorforum.com provides multiple question and answers and case study on different topics. Keep visiting auditorforum.com for more knowledge on analytical procedures.

{kind=link}