A chartered accountant is required to comply with five fundamental principles specified by Code of Ethics. However, compliance with the fundamental principles may potentially be threatened by a broad range of circumstances.

Required:

Briefly describe the categories of threats that may potentially affect compliance with the fundamental principles. Give two examples for each category.

Following are the categories of threats that may potentially affect the fundamental principles:

Categories of threats

[wpipa id=”617″]

(i) Self-interest threats: This may occur as a result of the financial or other interests of a chartered accountant or of an immediate or close family member.(Self Interest Threat to Auditor and related Safeguards)

- A financial interest in a client or jointly holding a financial interest with a client

- Undue dependence on total fees from a client

- Having a close business relationship with a client

- Concern about the possibility of losing a client

- Potential employment with a client

- Contingent fees relating to an assurance engagement

- A loan to or from an assurance client or any of its directors or officers

(ii) Self-review threat: This may occur when a previous judgment needs to be re-evaluated by the chartered accountant responsible for that judgment.(Self Review Threat with examples and real life situations)

- The discovery of a significant error during a re-evaluation of the work of the chartered accountant in practice

- Reporting on the operation of financial systems after being involved in their design or implementation

- Having prepared the original data used to generate records that are the subject matter of the engagement.

- A member of the assurance team being, or having recently been, a director or officer of that client

- A member of the assurance team being, or having recently been, employed by the client in a position to exert direct and significant influence over the subject matter of the engagement

- Performing a service for a client that directly affects the subject matter of the§ assurance engagement

[wpipa id=”617″]

(iii) Advocacy threats: This may occur when a chartered accountant promotes a position or opinion to the point that subsequent objectivity may be compromised.(Advocacy threat with examples and related safeguards)

- Promoting shares in a listed entity when that entity is a financial statement audit client.

- Acting as an advocate on behalf of an assurance client in litigation or disputes with third parties

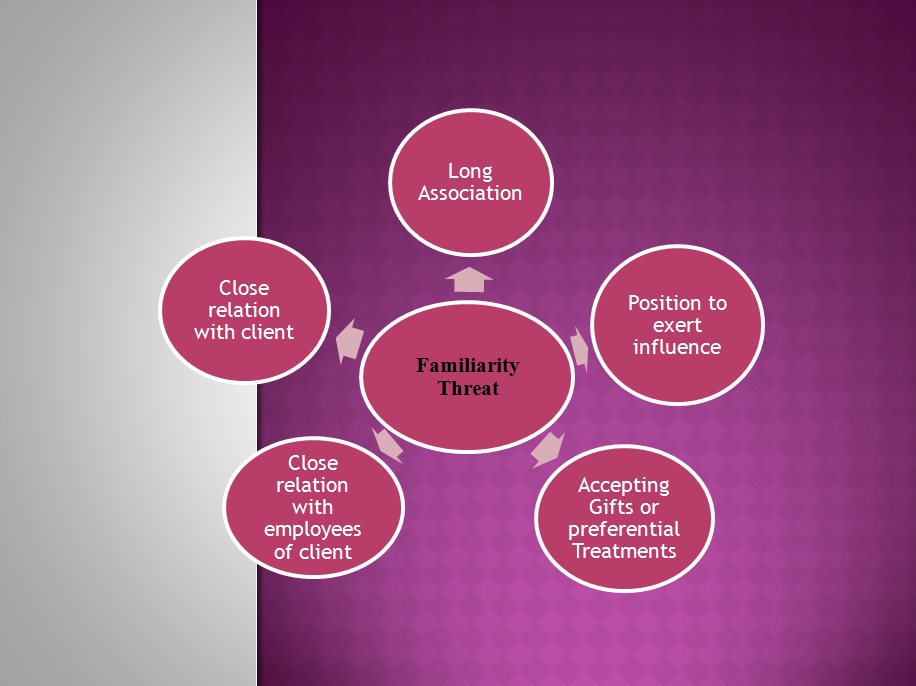

(iv) Familiarity threats: This may occur when, because of a close relationship, a chartered accountant becomes too sympathetic to the interests of others.(Familiarity Threat to auditor and related Safeguards)

- A member of the engagement team having a close or immediate family relationship with a director or officer of the client

- A member of the engagement team having a close or immediate family relationship with an employee of the client who is in a position to exert direct and significant influence over the subject matter of the engagement

- A former partner of the firm being a director or officer of the client or an employee in a position to exert direct and significant influence over the subject matter of the engagement

- Accepting gifts or preferential treatment from a client unless the value is clearly insignificant

- Long association of senior personnel with the assurance client

[wpipa id=”617″]

(v) Intimidation threats: This may occur when a chartered accountant may be deterred from action objectively by threats, actual or perceived.(Intimidation threat with examples and related safeguards)

- Being threatened with dismissal or replacement in relation to a client engagement

- Being threatened with litigation

- Being pressured to reduce inappropriately the extent of work performed in order to reduce fees.

For more practicing questions and answers related to threats and safeguards in real life situations explore auditorforum.com We are keen to know your views in comments.

{kind=link}